You, as an employer, often have direct control over your workers’ compensation program and its premiums. If you understand the broader concepts of workers’ comp, you can work with your insurance agent or broker to manage employee injuries in a manner that benefits the employee and keeps costs down.

There are two different types of claims costs: medical expenses and indemnity. The latter includes lost time wages and anything other than medical costs. It’s this latter element that you can control. The simplest way to do so is to place an injured employee in a light-duty work program in which the injury does not interfere with the work, and which the employee can perform during recovery. This keeps the employee involved in the business, and can decrease the impact on your workers’ comp premiums—in some cases by tens of thousands of dollars.

To help you understand how, let me introduce you to the “experience modification factor.” This is based off your most recent three years of workers’ compensation losses, excluding the most immediate policy year. For example, the 2017 experience mod would take into account the years 2013, 2014, and 2015. The lower the mod factor, the better.

Workers’ comp premiums are based on average claims costs for workers doing similar, or equally risky, work. If you have a .75 experience modification factor—signifying lower than average claims—your premium is determined by multiplying .75 times the base workers’ compensation premium, giving you a 25 percent discount. Conversely, if your experience mod is 1.25, you will pay a 25 percent surcharge.

Claims Costs: There’s a big difference between the impacts of medical and indemnity costs on your insurance premiums. If you can return an injured employee to work before the waiting period ends (usually three or seven days after an accident, depending on the state), and thus limit a claim to “medical only,” you get a 70 percent reduction when that claim is applied to your experience modification factor. As soon as the first dollar of indemnity expense is paid, you lose that 70 percent discount.

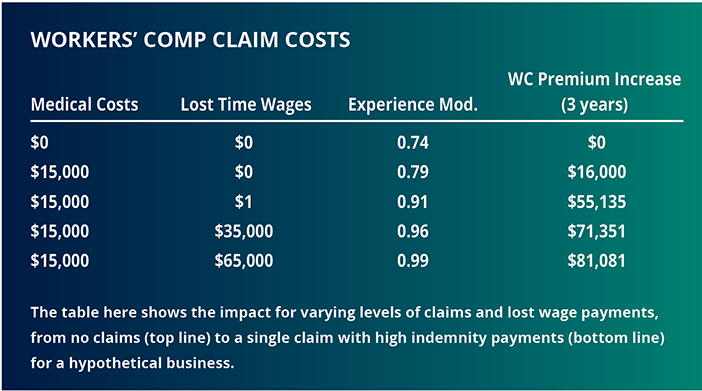

Take the example of a company that pays an estimated $80,000 in workers compensation and has a .74 experience mod (see chart, above right). If it has just one claim of $15,000 limited to medical expenses only, the claim’s effect on the experience mod takes it from .74 to .79. Over three years, the company’s workers compensation premiums will increase $16,000. Remember, because this claim was limited to medical expenses only, the claim received a 70 percent discount when it was applied to the experience mod.

If the employee is out of work for even a day longer than the waiting period, the injured employee would begin collecting lost time wages. This is an indemnity expense rather than a medical expense. In this case, the experience mod rises to .91 or more, and the company pays an additional $55,000 (or more) in increased premiums. In this instance, even $1 in lost-time wages would cost the company $39,000 in premiums over three years. That initial $1 of indemnity expense causes the biggest increase in the insurance premium, but the longer the employee is collecting lost time wages, the higher the mod factor and the insurance premiums.

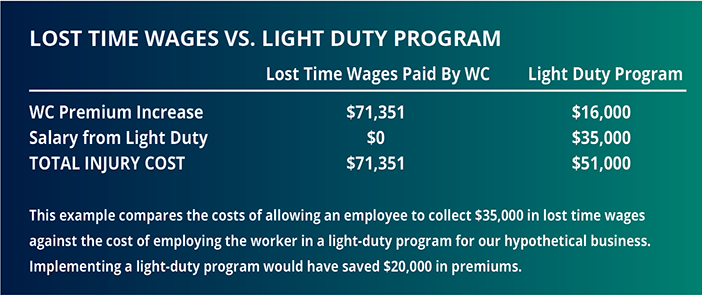

As a practical matter, the workers’ comp premium increase, once lost time wages are paid, will almost always exceed the cost of employing a worker in a light-duty program.

How To Prevent And Manage Lost Time Wages

When managing your experience mod and workers compensation premiums, there are two very important elements to consider.

1. Medical Provider Selection. If your state allows it, your company should have a pre-selected medical provider for employee injuries. This medical provider should be familiar with your operation and job descriptions. The medical provider should know that it is extremely important for you to get your employee back to work in a light-duty program as soon as possible, and know which jobs an injured employee is able to perform.

Why is this important? A doctor who is not familiar with your business (or who is a friend of the employee) might keep your employee home and out of work for an unnecessarily long time. That would cause your workers’ compensation premiums to rise.

2. Light-Duty Program. If an injured guide cannot do his normal job, a light-duty program can be a great way to keep him or her active in the company and allow you to retain the 70 percent discount on the claim. Have the injured guide help out in the office, at the reservations desk, or in another job function that does not require a lot of physical activity. This arrangement will help boost the employee’s morale and keep him or her part of the team. It will also encourage a fast recovery: Many guides would rather be in a more active role, and performing light-duty work may remind them they prefer being a guide.

The first step is to determine the length of the waiting period for lost time wages to be activated in your state. The employee needs to be in a light-duty program before missing this number of workdays, or you will lose the 70 percent discount that is applied when the claim is limited to medical expenses. The second step is to keep the employee busy with light-duty tasks. Both you and your employee will be glad you did.

{kind=link}